08/04/2025

On March 18, 2025, the Federal Government submitted Bill No. 1.087/2025 to the National Congress for review. The purpose of the proposed Bill is to amend the income tax legislation to establish a reduction in the tax liability on both the monthly and annual calculation bases, as well as to introduce a minimum tax rate for individuals allegedly earning high incomes.

In summary, the Bill proposes the following:

Reduction of Personal Income Tax (IRPF)

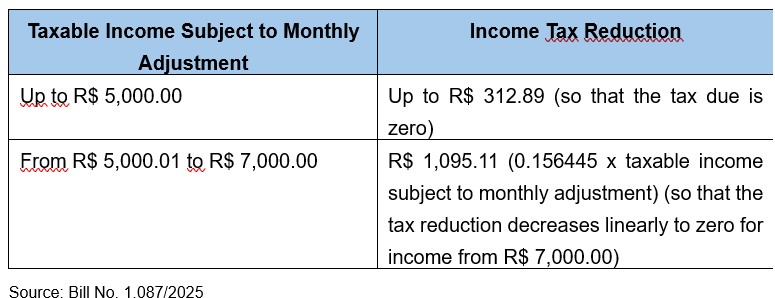

Bill No. 1.087/25 provides for a reduction of the Personal Income Tax (IRPF) to zero for individuals earning a taxable income subject to monthly adjustments of up to R$ 5,000.00.

In the case of taxable income subject to monthly adjustments from R$ 5,000.01 to R$ 7,000.00, an additional reduction has been introduced to minimize the incidence of the IRPF, as per the table below. In practice, this results in a significant loss of the progressivity of the tax rates in the IRPF:

Individuals with taxable income above R$ 7,000.00 will remain subject to the progressive IRPF table currently in force, without additional reductions.

Monthly Taxation of High Income

Bill No. 1.087/25 also provides that payments, credits, distribution, or delivery of profits or dividends by a legal entity to an individual resident in Brazil exceeding R$ 50,000.00 in a single month shall be subject to withholding of the Minimum Personal Income Tax (IRPFM) at a rate of 10% on the total amount paid, credited, or delivered, without any deductions.

Annual Taxation of High Income

Bill No. 1.087/25 establishes that an individual receiving total income exceeding R$ 600,000.00 within the calendar year will be subject to the IRPFM. It is important to note that in this case, all income received during the calendar year is considered, including those taxed exclusively or definitively, as well as exempt income or income subject to zero or reduced rates. The following deductions will apply exclusively:

- Capital gains, except those arising from transactions on the stock exchange or organized over-the-counter market subject to taxation based on net gains in Brazil;

- Income received in accumulated form exclusively taxed at source under Article 12-A of Law 7.713/88 (such as income paid as a result of judicial proceedings concerning several monthly periods), provided the taxpayer has not opted for its taxation in the Annual Adjustment Declaration;

- Amounts received by donation in anticipation of the legitime or inheritance.

It is worth mentioning that the IRPFM rate will be set based on the income assessed, with the following:

Moreover, the calculation base for the IRPFM will correspond to the assessed income, excluding exclusively:

- Income earned from savings accounts;

- Amounts received as compensation for work-related accidents, for material or moral damages, excluding lost profits;

- Exempt income; and

- Income from securities and financial assets exempt or subject to a zero tax rate, except income from stocks and other equity interests.

Taxation of Dividends Paid to Individuals Resident in Brazil

Bill No. 1.087/25 also establishes that if the sum of the effective tax rates on the legal entity’s profits, combined with the effective IRPFM rate applicable to the individual recipient, exceeds the nominal rates of the Corporate Income Tax (IRPJ) and the Social Contribution on Net Profit (CSLL), the Executive Branch will grant a reduction in the IRPFM calculated on the profits and dividends paid, credited, distributed, or delivered by each legal entity to the individual subject to the annual IRPFM.

The sum of the nominal rates to be considered for the above-mentioned limit is:

- 34% for general legal entities;

- 40% for insurance companies, capitalization companies, and entities regulated by the Central Bank; and

- 45% for financial institutions.

The value of the reduction specified in Bill No. 1.087/2025 will correspond to the result obtained by multiplying the amount of profits and dividends paid, credited, distributed, or delivered to the individual by the difference between: (i) the sum of the legal entity’s effective tax rate on profits and the effective IRPFM rate applicable to the individual recipient; and (ii) the legal entity’s tax rate (34% for general legal entities, 40% for entities regulated by the Central Bank, or 45% for financial institutions).

Taxation of Dividends Paid to Non-Residents

Furthermore, Bill No. 1.085/25 amends Article 10 of Law 9.249/95, establishing those profits or dividends paid, credited, distributed, delivered, or remitted abroad will be subject to withholding income tax (IRRF) at a rate of 10%.

If the sum of the effective IRPJ and CSLL rates of the legal entity paying the profits and dividends, combined with the 10% rate, exceeds the tax rate of the legal entity (34% for general legal entities, 40% for entities regulated by the Central Bank, or 45% for financial institutions), the Executive Branch will grant a credit to the non-resident beneficiary, calculated on the amount of profits and dividends paid, credited, distributed, delivered, or remitted that were subject to IRRF.

Bill 1.085/25 deserves criticism on several aspects, such as (i) eliminating the already low progressivity present in the IRPF, and (ii) introducing a model that seeks to tax dividends without providing any relief in corporate income taxation, putting foreign investment in Brazil at risk. It is important to note, however, that the Bill is still very recent and will undergo discussions in the National Congress, which may alter its final content.

Our Tax and Estate Planning, Family, and Succession teams are available to provide clarification and guidance on the subject.

Authored by: Thais Ribeiro Bernardes Casado